Exclusive: How blockchain is processing $1 million worth of ATM transactions daily in Nigeria

The Central Bank of Nigeria (CBN) further intensified its plans to transition the country into a cashless economy just before the end of 2022. It began in October by announcing what would be a heavily-criticized redesign of three of the highest currency denominations in the country — N200, N500 and N1,000. The bank went further on Dec. 6 by limiting cash withdrawals to a weekly maximum of N100,000 and N500,000 for individuals and corporate entities, respectively. It later revised the limits upward following more reprehension.

The problem?

There is, of course, the part that many residents particularly dislike the CBN — perhaps for its near-authoritarian methods. Just below that is the reality that Nigeria’s payment infrastructure isn’t robust enough to power a cashless economy. Failed electronic transactions are a norm across most channels, including internet banking, automated teller machines (ATMs) and point of sale (POS) terminals. It gets worse during holidays, which usually come with transaction spikes. A recent BusinessDay report narrates Nigerians’ disappointing experiences with electronic payment channels (e-channels) during the last Christmas holiday.

Blockchain could be a solution.

That’s part of what the team at Zone Network aims to achieve with its regulated blockchain protocol, which currently handles some ATM transactions for four Nigerian banks. Those banks include First City Monument Bank, Guaranty Trust Bank, United Bank for Africa and Zenith Bank.

Zone built its product on the Hyperledger Fabric, an open-source, enterprise-grade blockchain framework. Unlike public blockchains like Ethereum on which anyone can build without permission, participants in any Hyperledger Fabric-based network do in fact need to be given access to use or build on the protocol.

On Dec. 30, 2022, during the peak of the last holidays, Zone facilitated N408,691,500 — nearly $1 million — in ATM transaction volume for the four banks, according to data seen by Mariblock on the company’s Datadog-hosted live analytics dashboard. The transaction count was approximately 50,000.

This comes just about two months after taking its blockchain network into production. There are over 10 other banks currently using the network in a test environment.

For the entirety of December, the company did a transaction volume of roughly N6.44 billion ($14.3 million) across nearly 797,000 transactions.

But the figures above don’t mean much on their own. For one, the volumes quoted above are only a fragment of the overall ATM transaction volume countrywide.

Contexts, however, make them more palpable. At a base level, Zone couldn’t process those transactions without a switching license. In essence, blockchain is being used as a payment switch in Nigeria.

A switching company facilitates payment-related communication among different payment service providers. Nigeria’s leading switching companies include Nigeria Inter-Bank Settlement System Plc (NIBSS), Interswitch and Flutterwave.

More fascinating is the high success rates of the transactions, which is where the blockchain opportunity lies. The live data seen by Mariblock shows a 97.75% success rate on the acquiring banks’ side and 99.71% on the issuing banks’ side of the transactions.

The lower success rate on the acquirer side relative to the issuing banks is a result of network latency between the ATM and the infrastructure of the acquiring bank, Cofounder Elendu Uche told Mariblock. Network latency, in this context, occurs when the ATM cannot communicate quickly enough with the bank’s core infrastructure, from where the transaction request will be relayed to the switch.

“Sometimes, that delay can cause the transaction to take longer than the ATM’s expected processing time, which then leads to a failed transaction,” said Uche.

Still, it’s a marked improvement on what is seen with legacy switches.

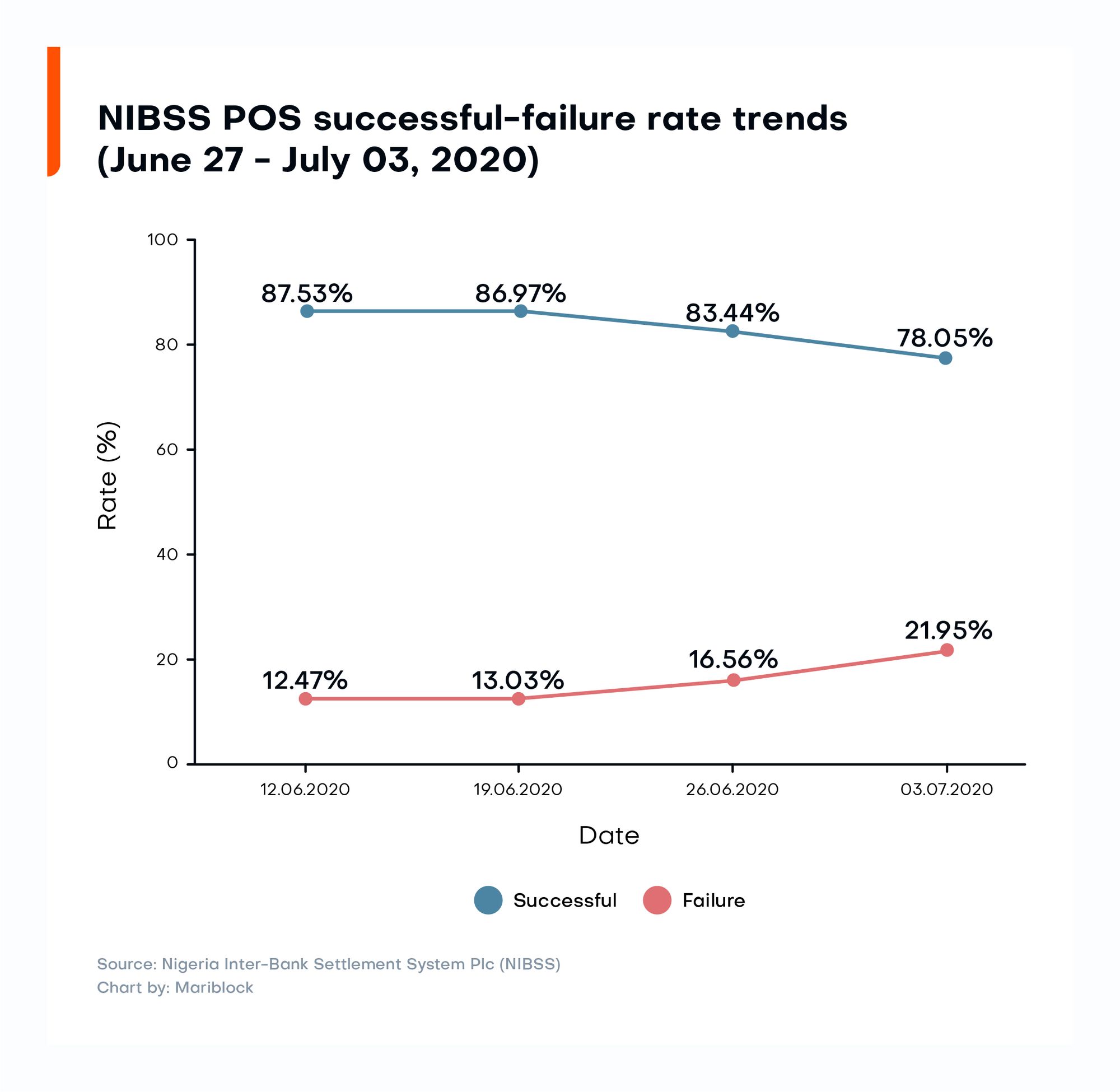

“The failure rate is 12% from the other guys [i.e., traditional processors such as Interswitch] as of when we engaged the banks to find out,” said Uche. “They say they’re seeing [a success rate of] between 87% and, on a very good day, 91%.”

The 12% failure rate Uche quoted is in line with previous figures for other payment switches. The chart that follows from nearly three years ago shows circa-12% failure rate has been isn't new.

However, the high failure rate with other switch operators isn’t always their fault. Industry professionals told Mariblock that banks and other payment gateways tend to experience glitches more frequently than the switch.

The approximately 12 percentage point improvement that Zone’s blockchain solution offers represents time and cost savings related to dispute resolutions, which itself is three-pronged. Lower dispute means improved customer experience, shorter time spent on resolutions, and lesser burden on the dispute resolution team.

The banks in Zone’s network, seeing these benefits, are now asking to onboard more transaction types (e.g., POS, funds transfer, etc.) to its platform, Uche told Mariblock.

“There are back and forth conversations with [some] divisional heads [at those four banks] asking us to start processing more categories of transactions because it’s saving them cost … the number of dispute issues they’re having is [shrinking].”

Zone’s blockchain-based switching solution, Uche said, currently processes between $400,000 and $600,000 worth of ATM transactions daily — depending on what’s going on in the country. Salary weeks tend to bring higher volumes.

How payment switching on blockchain works

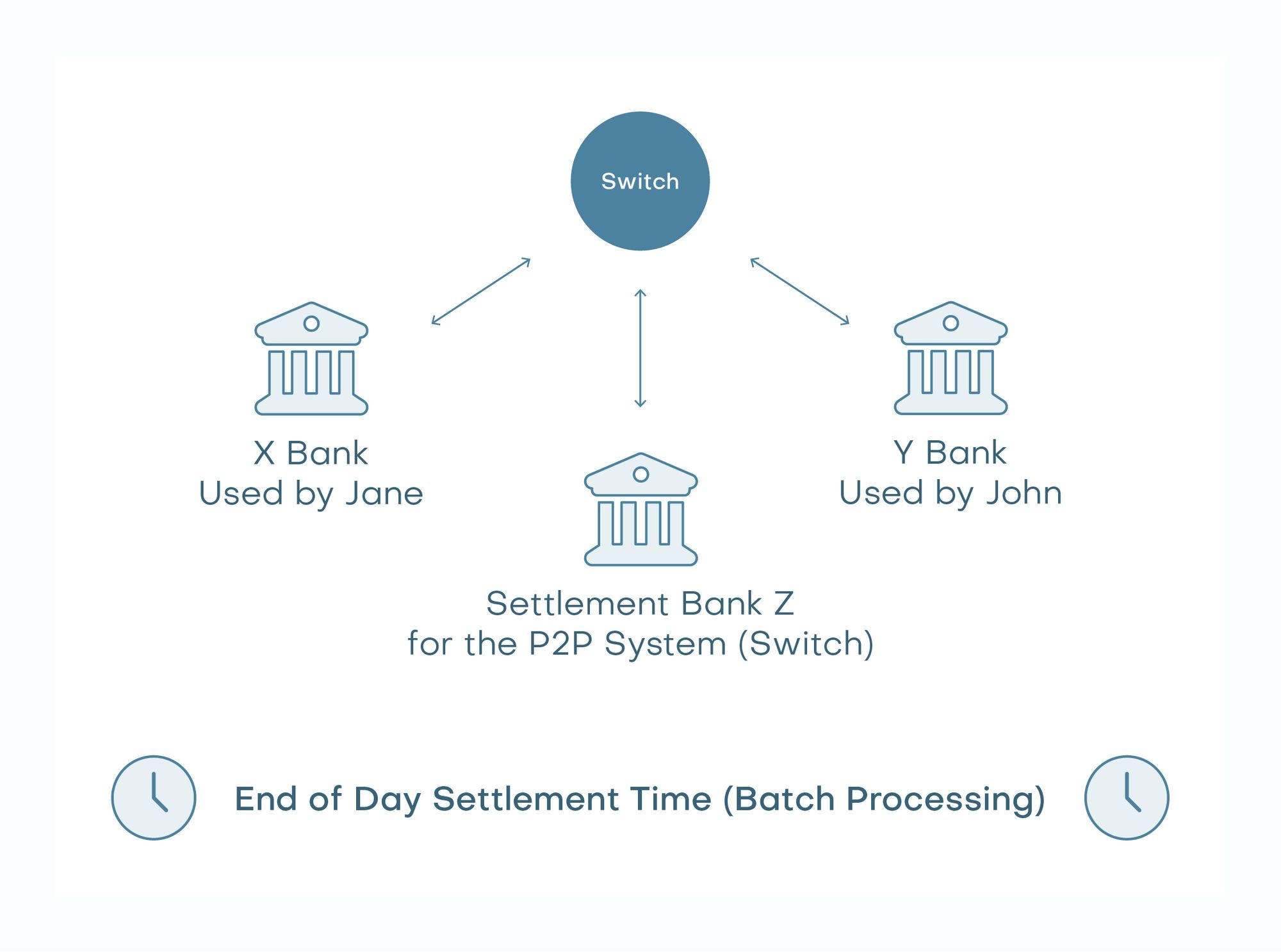

Traditionally, electronic transactions involving different payment service providers route through a centralized switch. The switch quintessentially receives a transaction instruction from an acquirer (e.g., a POS terminal) and relays it to the issuer (e.g., the bank that issued the customer a debit card). The issuer confirms the transaction’s validity and sends an approve or decline instruction back to the acquirer through the switch.

Failed transactions happen when there’s a break or delay in communication anywhere along the flow.

The communication failure can come from:

- A failure from the issuing bank’s infrastructure hindering its ability to return a message to the switch within the allotted time.

- The switch experiencing a downtime stopping it from relaying messages.

- A network failure at the acquiring bank such that it couldn’t receive a status message.

“Usually, what happens when you have problems with failed transactions is that the transaction says successful because you’ve been debited, but the receipt says failed because maybe a network outage or something happened before it got back to the terminal,” Zone CEO Obi Emetarom, told Mariblock.

“To resolve this, banks take days or weeks because your bank, the issuer bank, has the success status on its end. The switch may or may not have success on their end, and the acquirer bank has failed on their end. So now there’s a manual reconstitution that has to happen across these three parties before you get a refund. In the meantime, your money is stuck somewhere.”

With its blockchain-based solution, Zone claims to have reinvented the payment switching process for greater efficiency by allowing payment providers to interact in a peer-to-peer fashion — starting with ATM terminals.

“All of our participating banks have a node deployed within their environment. That node is connected to the ATM through some middleware, called a front-end processor (FEP) that connects the node to the ATM,” Emetarom said.

“So essentially, when you take your card to another bank’s ATM that has the blockchain node deployed, and you do a transaction, the ATM sends the transaction to the node within the bank, and that node forwards that transaction straight to the node sitting in your bank.

“From there, there’s a debit passed [onto] your account from the core banking application and a response all the way back to the ATM that this transaction is successful. Then you get paid.

“What that means is it bypasses a central switch hub on the one hand. On the other hand, the settlement and reconciliation process [are] handled on the blockchain. So records required for settlement sit on both banks’ sides — the acquiring and issuing banks. And those records are the same.”

Zone’s blockchain also features a smart contract-like tool that facilitates automatic reversal when a user gets debited without receiving value.

“What we also do to help reconciliation for situations where you’re debited and the ATM sort of displays a failure, but you’ve already been debited, is that we also get the final state of that transaction — the digital version of the receipt is also sent to the blockchain and stored on both sides. So now the blockchain has the transaction status and the receipt.

“Because the [nodes] across both banks have a copy of both the transaction status and the receipt … once the system sees a deviation, meaning the transaction status says successful, and the receipt says failed, we don’t need to wait for you to complain to your bank. The system would auto-reverse that transaction, and the reconciliation [would be] done instantly.

“Once we see what the system sees, a deviation, meaning the transaction was successful [but] the receipt says failed, we don’t need to wait for you to complain to your bank. The system would auto-reverse.”

Though intriguing, blockchain does not — and almost certainly will not — fix electronic payments beyond making the existing process more efficient. For one, there are scads of potential points of failure within the infrastructure of each entity involved in the payment way before blockchain comes in. As Uche alluded, ATMs sometimes experience difficulties communicating with the main bank infrastructure. Zone’s blockchain does not fix that.

“We’ve found that the weakest links for our infrastructure are the banks,” Uche said, “From time to time, the network infrastructure within banks goes down.”

Zone may not be the only Nigerian switch provider using blockchain for much longer. Interswitch, a larger and more established competitor, is working with enterprise blockchain project Interstellar to “develop blockchain-powered infrastructure services and solutions.”