The Nigerian government is unwittingly driving crypto adoption

Nigeria's apex bank recently limited cash withdrawals in a display of excessive force. It leaves citizens at the mercy of banks to access their money.

- The Central Bank of Nigeria (CBN) has updated cash withdrawal limits. Individuals and corporate organizations can now withdraw up to a weekly limit of ₦500,000 weekly and ₦5,000,000, respectively.

- The CBN still leaves customers at the mercy of financial institutions to decide if their reasons are good enough to withdraw cash above those limits.

The Central Bank of Nigeria (CBN), in a bid to promote a cashless economy, has ordered all deposit-accepting financial institutions to deny customers access to withdrawals beyond specific amounts. A part of the new policy, issued on Dec. 6, hands banks disproportionate power to decide if customers’ reasons are “compelling” enough to exceed those limits. This highlights the CBN’s tendency to play God and is partly why Nigeria ranks high for grassroots cryptocurrency adoption.

Details on the new policy

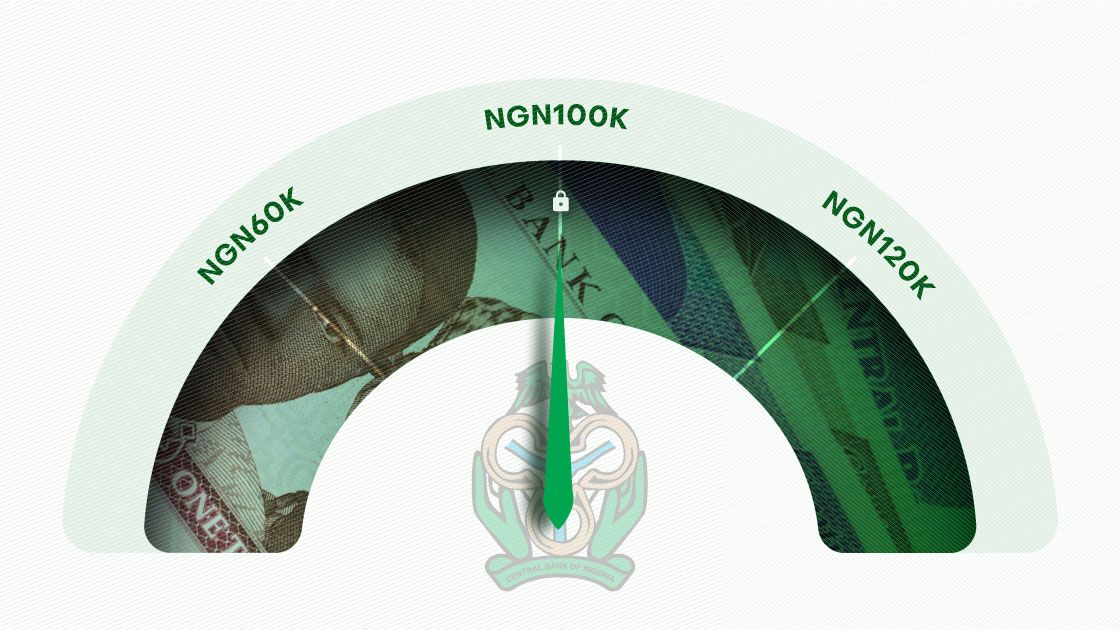

- Banks are to limit over-the-counter cash withdrawals to a weekly maximum of ₦100,000 ($226) and ₦500,000 ($1,129) for individuals and corporate entities, respectively. Withdrawals exceeding these limits will attract a 5% processing fee for individuals and 10% for corporate organizations.

- Automated Teller Machine (ATM) cash withdrawals now have a limit of ₦20,000 ($45) daily and ₦100,000 per week. The CBN also directed banks to load ATMs with denominations no higher than ₦200.

- In addition, Point of Sale (POS) cash withdrawals now have a limit of ₦20,000 per day. Nigeria’s burgeoning agency banking space relies on the use of POS devices. Although customers will still be able to conduct cashless transactions with POS terminals, it’s unknown whether the CBN’s latest policy will be well-received.

- According to journalist Abubakar Idris, “Agency banking is the biggest loser [of] the new CBN policy. And then there’s financial inclusion which could suffer a second-order effect. Meanwhile, e-channels (especially for small businesses) still have a long way to go. Things could change fast, though.”

Agency banking is the biggest loser with the new CBN policy. And then there's financial inclusion which could suffer a second order effect.

— Abubakar (@IAtalkspace) December 6, 2022

Meanwhile, e-channels (especially for small businesses) still have a long way to go. Things could change fast though... https://t.co/Wq7cBzDGEg

Perhaps the most controversial aspect of the directives is that, even when a customer is willing to incur the stipulated fee for exceeding those limits, the bank must first ascertain if the customer has a strong reason. Even then, it can’t be more than once a month.

Telling quote

“In compelling circumstances, not exceeding once a month, where cash withdrawals above the prescribed limits [are] required for legitimate purposes, such cash withdrawals shall not exceed ₦5,000,000.00 and ₦10,000,000.00 for individuals and corporate [organizations], respectively, and shall be subject to the referenced processing fees … above, in addition to enhanced due diligence and further information requirements.”

Regulator — not God

To be clear, there are merits to CBN’s desire to transition Nigeria into a cashless economy. What is troubling is how it tends to develop new rules without giving much thought to the implications of human rights.

And yes, central banks’ choices to achieve their goals have human rights implications.

Daniel Bradlow, a professor of international development law and African economic relations at the American University Washington College of Law, wrote:

“Central banks cannot operate without having social impacts and thus without impacting human rights. [Therefore,] human rights [offer] central banks a new tool for understanding the true costs and benefits of their proposed actions as well as useful additional information that can help them identify ways to mitigate the adverse consequences of their action.”

The CBN most certainly knows this, and it begs the question of why the bank never seems to consult the public before making its decisions. If it does, it is not available in public domains. The central banks of countries like the United States and England routinely publish calls for comments on their respective websites.

The downside of CBN’s authoritarian approach to managing the Nigerian monetary system is that many citizens are left in the lurch. That is likely to happen with the latest CBN policy. Despite a growing electronic finance industry, many Nigerian citizens prefer cash.

A 2019 report from the United States Agency for International Development (USAID) found that only 16% of Nigerian adults that took part in the survey had made a digital payment in 12 months. That’s unlikely to have improved much. Consequently, a lot of cash-dependent citizens, a lot of whom are without bank accounts, could suffer.

And there is also the risk that the CBN’s latest policy will create a black market for the naira.

It is not the first time CBN has issued strict orders, which banks are predisposed to implement immediately for fear of sanctions. In Feb. 2021, the apex bank directed financial institutions to stop facilitating payments for crypto entities. A few months before that, the bank got approval to freeze the accounts of some individuals and public affairs companies linked to the viral “ENDSARS” protests of 2020.

This authoritarian approach to managing a monetary system is everything cryptocurrency exists to solve. It gives citizens the freedom to choose an alternative and permissionless way to store their money.

On the surface, the institution of withdrawal limits has nothing to do with crypto. But with the CBN putting customers at the mercy of banks to withdraw their hard-earned money in cash if they so desire, one has to ask just how far the apex bank would go to suppress people’s rights, all in the name of maintaining the monetary system.

Unsurprisingly, Nigeria is one of the world’s leaders in grassroots cryptocurrency adoption. Despite the bear market of 2022, crypto transaction volumes in the West African country continue to grow. That is mainly driven by the fact that crypto helps ease some of the systemic financial services challenges in the country.

For instance, an increasing number of Nigerians are turning to stablecoins — digital currencies designed to preserve a peg to the dollar — to hedge against currency depreciation. In the parallel market, the naira has lost over 20% of its value against the dollar over the last year.